/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

Apple (AAPL) is quietly setting up the next phase of its growth story. In the first half of 2027, it’s expected to launch a refreshed iPad Pro lineup along with a redesigned entry‑level MacBook Pro. These new devices will land at a key time for the company. That timing follows a strong fiscal 2026, when Apple posted a record $111.2 billion in Q2 revenue, helped by heavy demand for the iPhone 17.

This kind of performance is exactly why this next move matters so much for investors. Apple is at a size where every hardware update gets judged on whether it can still move the needle in a meaningful way.

The question now is simple but important. With new iPad Pro and MacBook Pro models reportedly on the way, is Apple just giving its familiar products another polish, or laying the groundwork for something bigger for AAPL holders?

Apple’s Premium Financials

Based in Cupertino, California, Apple designs and sells the iPhone, Mac, iPad, wearables and a wide range of software and services, giving it one of the most tightly integrated hardware and digital ecosystems in the world.

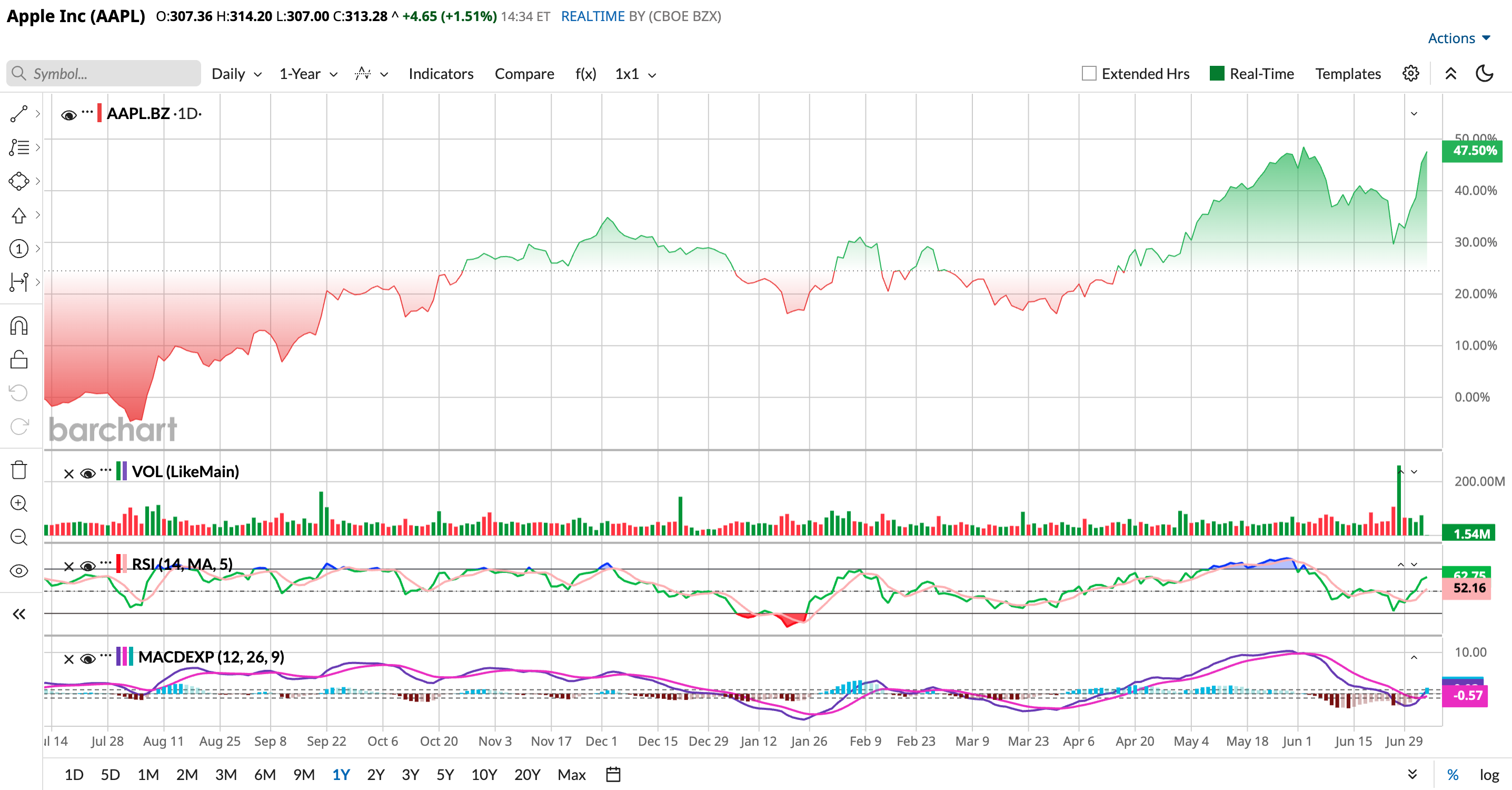

AAPL stock is up 14.96% year-to-date (YTD) and 46.35% over the past 52 weeks.

The stock is clearly priced at a premium. Its valuation sits at 37.32 times trailing price-to-earnings Non-GAAP and 10.11 times trailing sales, compared with sector medians of 26 times and 3.67 times. The company’s market capitalization is about $4.53 trillion, with a forward annual dividend of $1.08 per share, which translates into a modest 0.35% yield.

Apple reported fiscal 2026 second‑quarter revenue of $111.2 billion for the period ended March 28, 2026, up 17% year-over-year (YOY) and ahead of analyst expectations of $109.3 billion. The company also delivered diluted EPS of $2.01, up 22% and about 4.69% above consensus.

There are, however, some nuances in the headline profit figures. Reported net income for March 2026 was $29.58 billion, with net income growth of ‑29.74%.

At the same time, Apple’s margin profile moved in the right direction for a hardware‑heavy business, with gross margin rising to 49.3% from 47.1% and operating margin improving to 32.3% from 31%.

Cash generation ties the story together. Apple produced operating cash flow of $82.63 billion in March 2026, up 53.23%, and net cash flow of $9.64 billion, up 2.72%, giving it plenty of room to keep investing.

Apple’s Product Pipeline

Apple is lining up a busy 2027 on the hardware side, and the pieces fit together more than they might seem at first glance. The company is preparing four new iPad Pro models for spring 2027, along with a redesigned entry‑level 14-inch MacBook Pro for the first half of the year.

Apple’s new iPad Pro lineup should stick with the 11-inch and 13-inch sizes, with most of the change coming from internal upgrades rather than a fresh look. That naturally keeps attention on chip performance, battery life, and day‑to‑day experience rather than headline‑grabbing redesigns.

Those plans sit alongside a clear move up the pricing ladder. Apple has already raised prices on several Mac, iPad, and home products as memory and storage costs climb with stronger AI data center demand. The 14-inch MacBook Pro now starts at $1,999 instead of $1,699, and the 11-inch iPad Pro starts at $1,199 rather than $999.

On top of that, the iPhone roadmap gives the whole story more weight. Apple plans to launch five new iPhone models over the next 12 months, including its first foldable iPhone, which would mark a big shift in the lineup.

Suppliers have reportedly been told to prepare for 10 million foldable units this year, up from an earlier forecast of 7 million. The total iPhone output is expected to top 220 million units this year, more than double the roughly 100 million smartphones planned by Xiaomi, Oppo, and Vivo combined, which keeps Apple firmly in a different league.

Put together, these initiatives all point in the same direction, giving Apple several levers to keep hardware revenue growing even as it asks customers to pay more.

Analysts Still See Measured Upside

Wall Street’s attention is already shifting to Apple’s next update. The company is expected to report earnings on July 30, and the bar is not low. For the June 2026 quarter, consensus is looking for EPS of $1.88, up from $1.57 a year earlier, which works out to about 19.75% YOY growth.

Some houses think the story could run further than the near‑term numbers suggest. Bank of America analyst Wamsi Mohan recently lifted his price target to $380 from $330 and kept a “Buy” rating in place. His call leans heavily on “agentic” AI, in other words, AI features that can carry out tasks across apps, services, and devices with less user input, which he believes could deepen Apple’s ecosystem advantage.

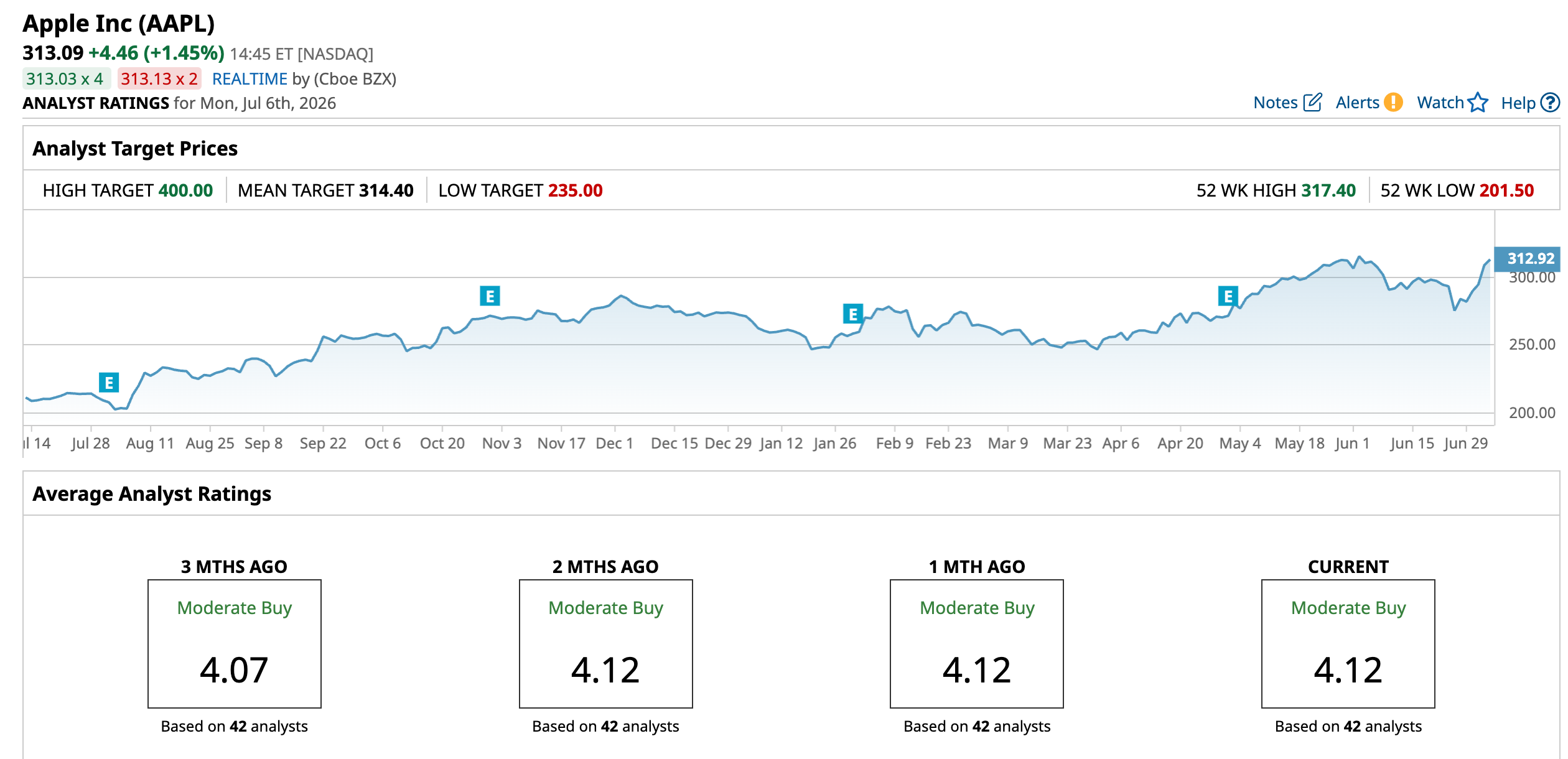

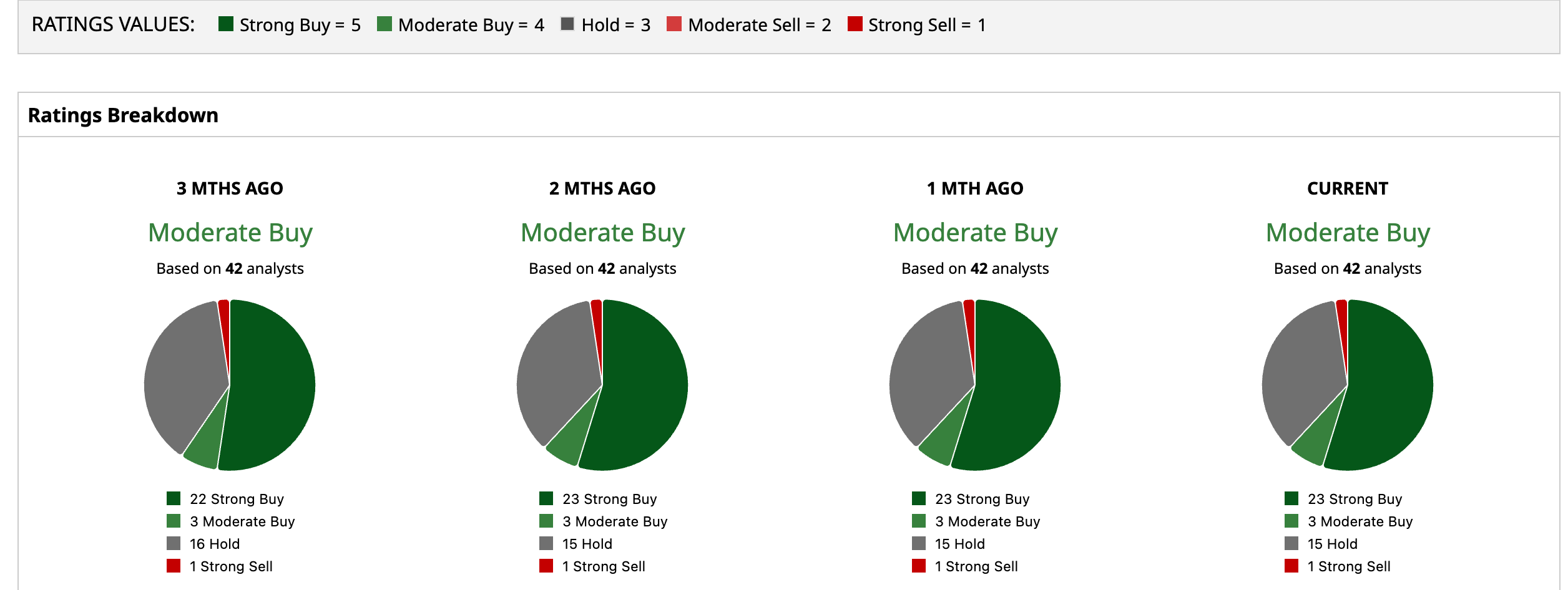

Overall sentiment stays positive, but not in an over‑the‑top way. The consensus rating on AAPL sits at “Moderate Buy,” based on 42 analyst opinions rather than a single, unanimous stance. The average price target is $314.40, implying a marginal upside, but the Street-high target price of $400 shows a potential climb of 27.8% over the next 12 months.

Conclusion

Apple’s planned 2027 iPad Pro and MacBook Pro updates look like solid growth support, but they do not seem big enough on their own to fully reignite AAPL. The stronger case for the stock still rests on AI features, services growth, and Apple’s ability to keep margins strong. Their shares look more likely to grind higher than break out sharply, especially if upcoming earnings stay firm and the 2027 product cycle continues to build momentum.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.